The Direct Message

Tension: The funniest person in a friend group is often the one carrying the most unacknowledged pain, because their humor creates an illusion of resilience that prevents anyone from checking on them.

Noise: Society classifies humor as a ‘mature’ defense mechanism and celebrates those who wield it, conflating comedic skill with emotional well-being and rewarding the performance that keeps the real person invisible.

Direct Message: The joke was never about making people laugh — it was about making sure they stayed. And the only person who knows the difference between genuine resilience and skilled deflection is the one who can’t stop performing.

Every DMNews article follows The Direct Message methodology.

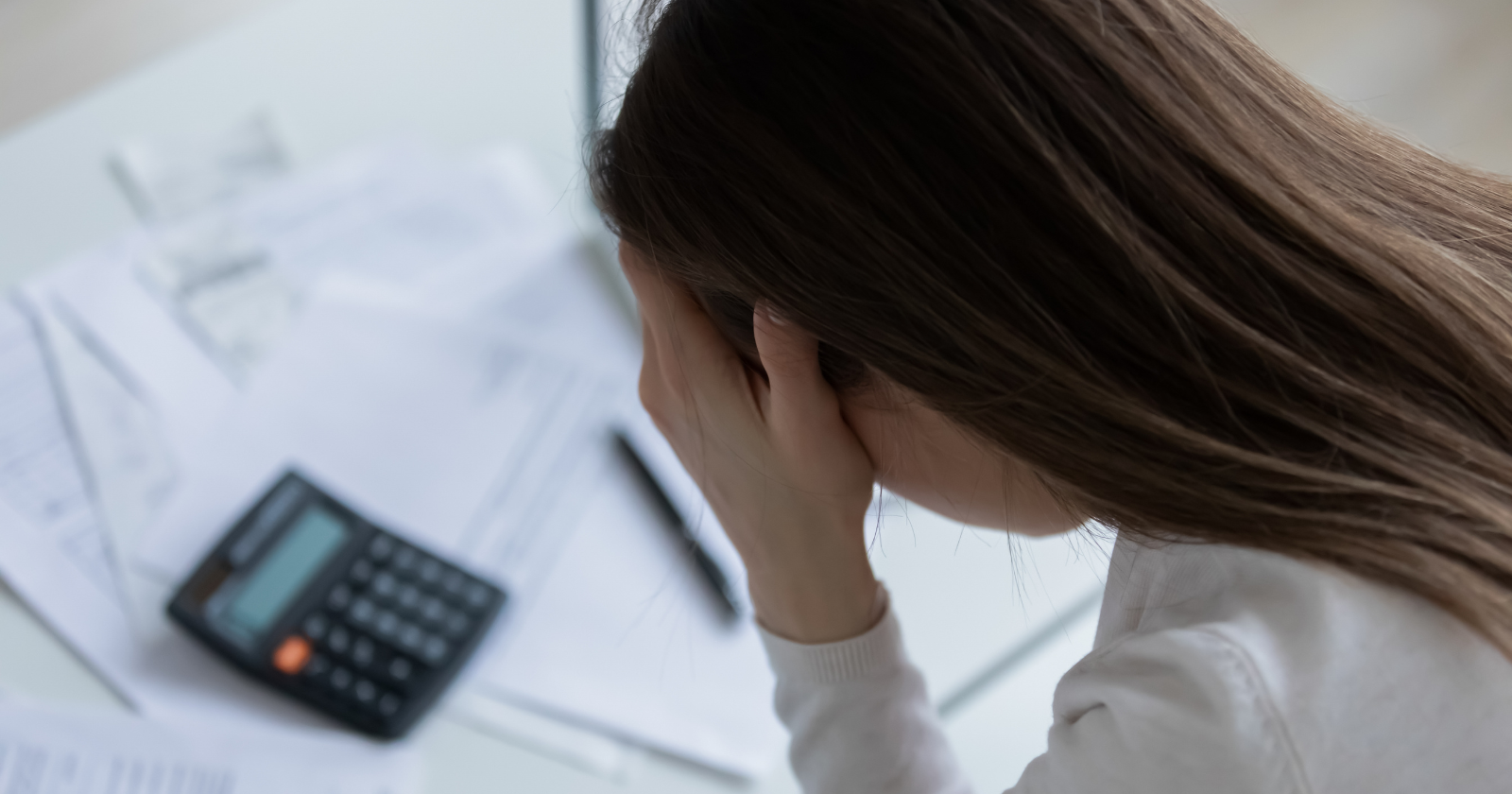

Picture this: You’ve finally made it. After years of hard work, your bank account has a comfortable cushion. You can afford that vacation, that nice dinner, that thing you’ve been eyeing for months.

But instead of feeling free, you feel anxious. Every purchase triggers a small panic. You check your balance obsessively, even though you know you’re fine. Sound familiar?

If you grew up in a household where money was tight, where every dollar was stretched, where financial stress hung in the air like smoke, then you know exactly what I’m talking about. The scarcity you experienced as a kid doesn’t just disappear when your circumstances change.

It follows you. It whispers in your ear when you’re about to buy something nice. It makes you feel guilty for enjoying what you’ve earned.

I’ve been thinking about this a lot lately, especially after a conversation with a friend who just got a significant raise but still shops like they’re making minimum wage. They know the numbers add up, but something deeper holds them back.

The brain remembers what the bank account forgets

Here’s what’s fascinating about our relationship with money: it’s rarely about the actual numbers in our account. It’s about the stories we’ve internalized, the patterns we’ve developed, and the survival mechanisms we built when we were young.

Growing up in Sacramento, I watched my parents run their small accounting practice from our home office. They understood numbers better than anyone, yet when their marriage fell apart when I was 14, I saw how emotional patterns could override logical thinking. Even people who work with money every day can struggle with their relationship to it.

Our brains are wired for survival, not abundance. When you grow up experiencing financial instability, your nervous system learns to stay on high alert. It’s constantly scanning for threats, preparing for the next crisis, even when there isn’t one coming.

Psychologists call this hypervigilance, and it served you well when resources were actually scarce. The problem? Your brain doesn’t automatically update its software when your circumstances change.

Think about it like this: if you spent years training for a marathon, your body wouldn’t suddenly forget how to run just because the race ended. The same goes for financial stress. Those neural pathways you built don’t disappear just because your paycheck increased.

The guilt that comes with having enough

One of the most unexpected challenges of financial stability after growing up without it? The guilt.

You might feel guilty for having more than your parents did. Guilty for not struggling the way they struggled. Guilty for enjoying something they couldn’t afford. This survivor’s guilt is real, and it’s more common than you’d think.

I remember working at a coffee shop in high school, watching customers drop $5 on a latte without thinking twice. Meanwhile, I was calculating how many hours of work that represented. Even now, years later, part of me still does that math.

There’s also the fear of becoming “one of those people” – the ones who forget where they came from, who lose touch with their roots. So you hold yourself back, keeping one foot in your old financial reality even as you’ve moved into a new one.

The waiting for the other shoe to drop

If you’ve experienced financial instability, you know that money can disappear as quickly as it appears. A medical emergency, a job loss, a car breaking down – you’ve seen how quickly things can unravel.

So even when things are good, you’re waiting. Waiting for the crisis. Waiting for the emergency. Waiting for proof that this stability is temporary, just like you always suspected it would be.

This creates a self-fulfilling prophecy of sorts. You can’t enjoy your money because you’re so focused on protecting it. You save obsessively, deny yourself pleasures you can afford, and live as if disaster is always around the corner.

During my years in digital marketing, I saw this pattern repeatedly among colleagues who’d grown up with less. Even those earning six figures would bring lunch from home every day, not out of preference, but out of deep-seated fear of spending.

Breaking the scarcity cycle

So how do you break free from these patterns? How do you learn to enjoy what you’ve worked so hard to achieve?

First, recognize that this is a process, not a switch you can flip. You’re essentially rewiring years or decades of conditioning. Be patient with yourself.

Start small. Pick one small luxury you can easily afford and practice enjoying it without guilt. Maybe it’s a nice coffee, a book you want, or a slightly fancier grocery item. Notice the resistance that comes up and sit with it.

Track your numbers regularly – not obsessively, but consistently. When you know exactly where you stand financially, it’s harder for your anxiety to convince you that you’re in danger. Facts can help counteract fear.

Consider working with a therapist who understands financial trauma. Yes, that’s a real thing, and it’s more common than you might think. The patterns we’re discussing here run deep, and sometimes professional help is the fastest path to healing.

Rewriting your money story

What if instead of seeing your caution around money as a weakness, you saw it as a strength that needs updating?

Your ability to be careful with money, to think twice before spending, to plan for contingencies – these are valuable skills. They got you to where you are now. The goal isn’t to abandon them completely but to recalibrate them for your current reality.

Start noticing the stories you tell yourself about money. Do you believe you don’t deserve nice things? That people like you don’t get to be comfortable? That financial security is for other people?

Challenge these beliefs. Write down evidence that contradicts them. Create new stories that acknowledge both where you came from and where you are now.

Putting it all together

At the end of the day, struggling to enjoy money after growing up without it isn’t a character flaw or a sign of ingratitude. It’s a normal response to early experiences that shaped your nervous system and worldview.

The path forward isn’t about forcing yourself to spend or shaming yourself for being cautious. It’s about slowly, deliberately teaching your brain that it’s safe now. That you can enjoy what you have while still being responsible. That abundance and security aren’t mutually exclusive.

Remember, you’re not trying to forget where you came from. You’re trying to integrate your past with your present, creating a relationship with money that honors both your history and your current reality.

This work takes time, and that’s okay. Every small step toward enjoying what you’ve earned is a victory. Every moment you allow yourself to feel secure is progress.

Your younger self worked hard to protect you. Now it’s time to gently show them that they can rest. You’ve got this covered.